What the Paperwork Says: Five Patterns Hiding in Epstein’s Corporate Web

A companion piece to “Epstein’s Financial Web.” That report is the reference document - every entity, every source, cited ad nauseam. This is the analysis: What all of that paperwork tells us when you take a step back and analyze the shape of it.

When I published my entity-by-entity breakdown of Jeffrey Epstein’s financial web, I promised documentation, not accusation. That’s still the deal. However, after cataloguing more than forty companies, trusts, and foundations - and reading more incorporation documents, annual reports, and bank subpoena returns than any person should - I can tell you that the documents have a shape. Corporate paperwork is supposed to be boring. This paperwork is boring on purpose, but the patterns in it are anything but.

Here are five of them. Everything below can be traced back to a specific document in the DOJ Epstein files (the EFTA series), a court record, or independently verified public reporting. Where something is an allegation rather than an established fact, I’ll say so.

1. Every asset got two companies - and someone wrote down why

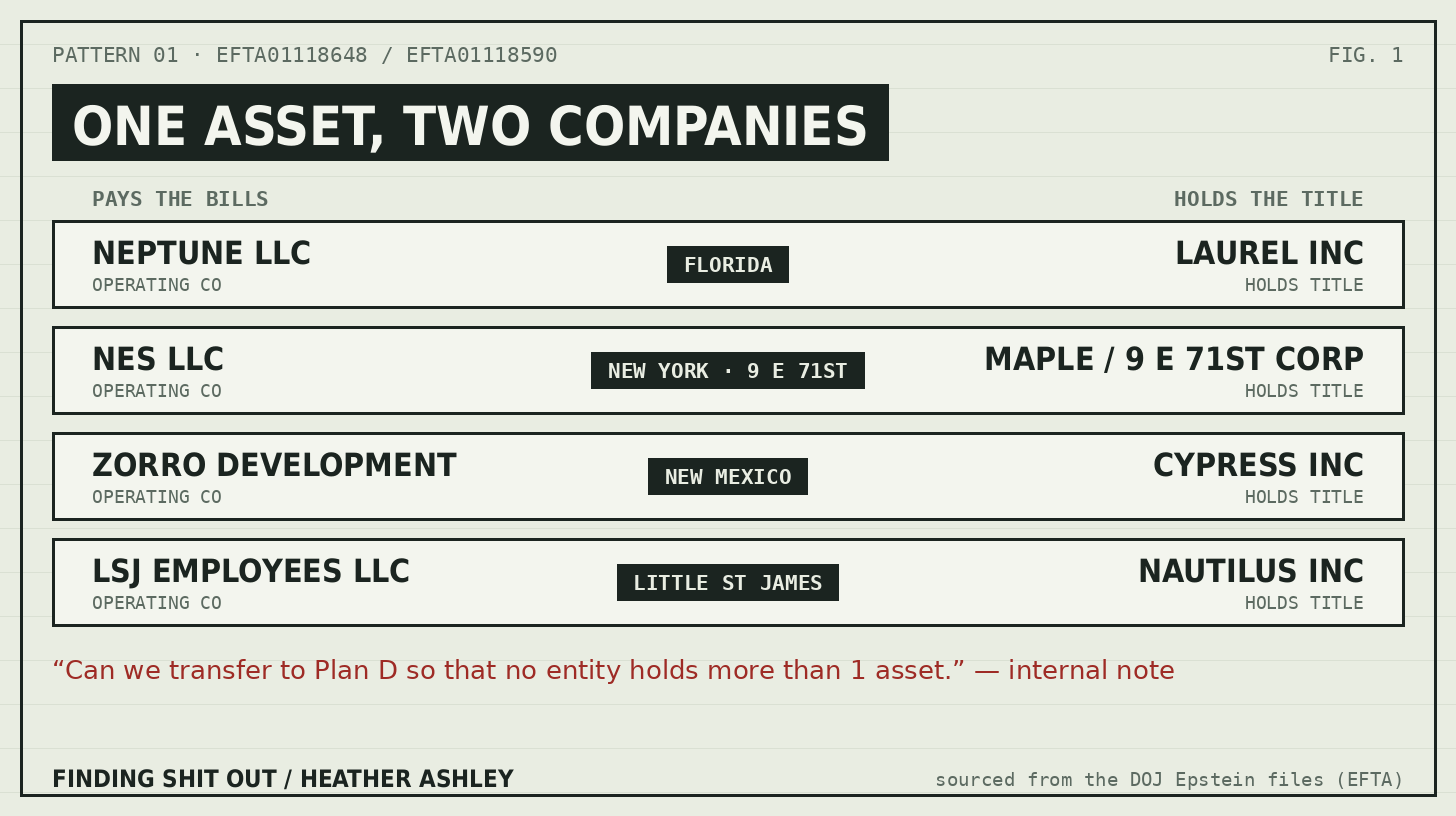

Scattered through Epstein’s internal financial notes (EFTA01118648, EFTA01118590) is the same question, asked property by property: should the operating company pay, or the title company?

Florida: Neptune LLC operates, Laurel Inc holds the title. New York: NES LLC operates, Maple Inc holds the title, with Nine East 71st Street Corp sitting under NES as the “no activity” title holder for the townhouse. - New Mexico: Zorro Development operates, Cypress Inc holds the title. - Little St James: LSJ Employees LLC operates, Nautilus Inc holds title.

This isn’t me inferring a strategy from a pattern. The strategy is written down. One note asks whether assets can be moved “so that no entity holds more than 1 asset.” That’s the whole architecture in eleven words: Fragment everything, so that no single company - and no single lawsuit, lien, or subpoena aimed at one - can touch more than one thing.

This is worth saying plainly: Layered holding structures are legal and common among the very wealthy. What makes this set worth documenting is what the structure was later alleged to have shielded, and how consistently the same fragmentation logic shows up across every property he owned.

2. The empire fit in one office suite

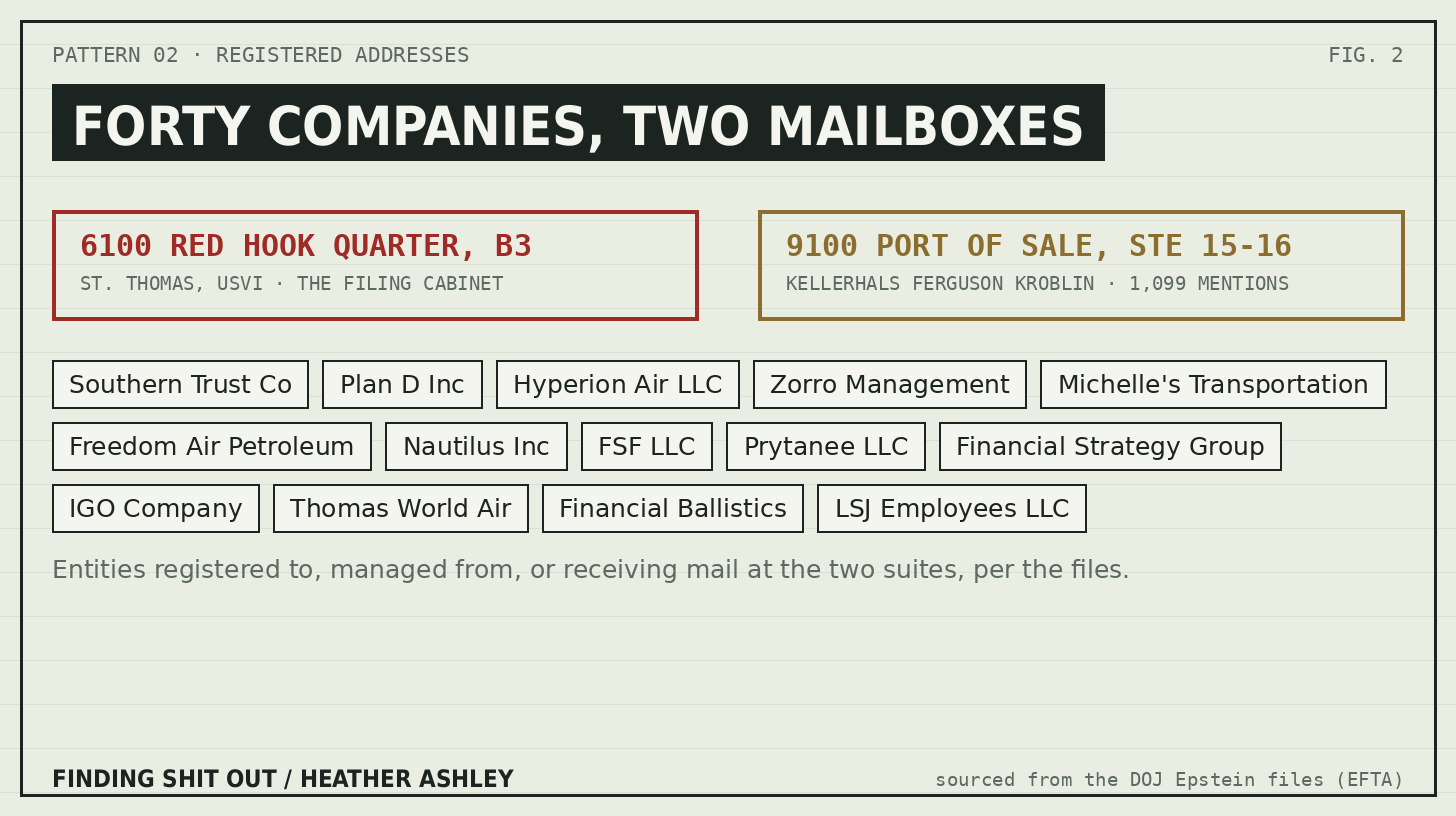

If you mailed a letter to 6100 Red Hook Quarter, Suite B3, St. Thomas, U.S. Virgin Islands, it could plausibly have reached Southern Trust Company, Plan D Inc, Hyperion Air LLC, Zorro Management, Michelle’s Transportation, Freedom Air Petroleum, Nautilus Inc, FSF LLC, Prytanee LLC, Financial Strategy Group Ltd, or the manager of record for several more.

That’s not a business district. That’s a filing cabinet.

A second address does similar work: 9100 Port of Sale/Havensight, Suite 15-16 - the offices of the law firm Kellerhals Ferguson Kroblin PLLC, which served as registered agent, incorporator, or mail drop across the web. The firm’s name appears 1,099 times in the Epstein files. Registered-agent work is a normal legal service; the volume is what tells you how centralized this supposedly sprawling “web” really was. Forty companies, two mailboxes.

3. It was never forty companies. It was one man and about six signatures

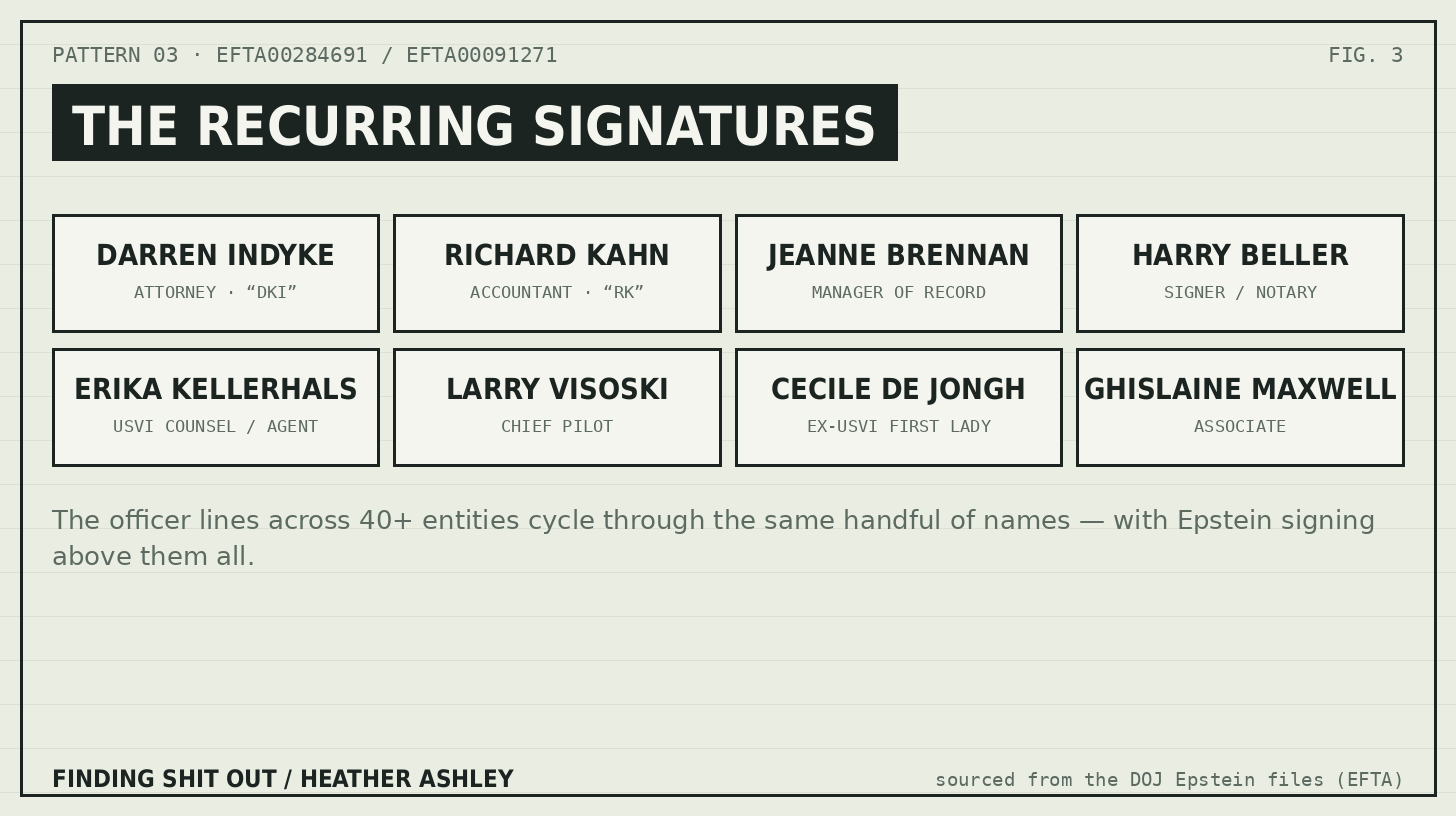

Pull the annual reports (EFTA00284691) and the FirstBank Puerto Rico subpoena returns (EFTA00091271) and the same names cycle through every officer line: Darren Indyke, attorney - “DKI” in internal shorthand. Richard Kahn, accountant - “RK.” Jeanne Brennan(-Wiebracht), the manager of record for entity after entity, always at that same Red Hook Quarter address. Harry Beller signing and notarizing. Erika Kellerhals as USVI counsel and registered representative. Larry Visoski - Epstein’s pilot for decades - listed as manager or member of the aviation companies.

There’s another name that deserves its own paragraph: Cecile de Jongh, who was First Lady of the U.S. Virgin Islands from 2007 to 2015. The files show her signature as Manager of Southern Trust Company on a purchase order (EFTA01221763) and list her as an officer and director of Financial Trust Company. She is listed as director of another company - Geepers Inc - in a separate Annual Report (EFTA00313135). Those are documented facts. Separately, in USVI v. JPMorgan, the bank alleged she managed Epstein’s USVI companies for two decades, earned $200,000 in 2007 alone, and served as his “primary conduit” for influence in the territory’s government. Those are allegations made in litigation - a defense filing, not a judicial finding - and she has testified she had no knowledge of his crimes. Both things belong in the record: The signatures are facts; the characterization is contested.

The takeaway either way: The “web” had no real web of people behind it. A structure this wide, run this narrow, means every thread was visible to a very small group.

4. The money is corroborated - three times over, and counting

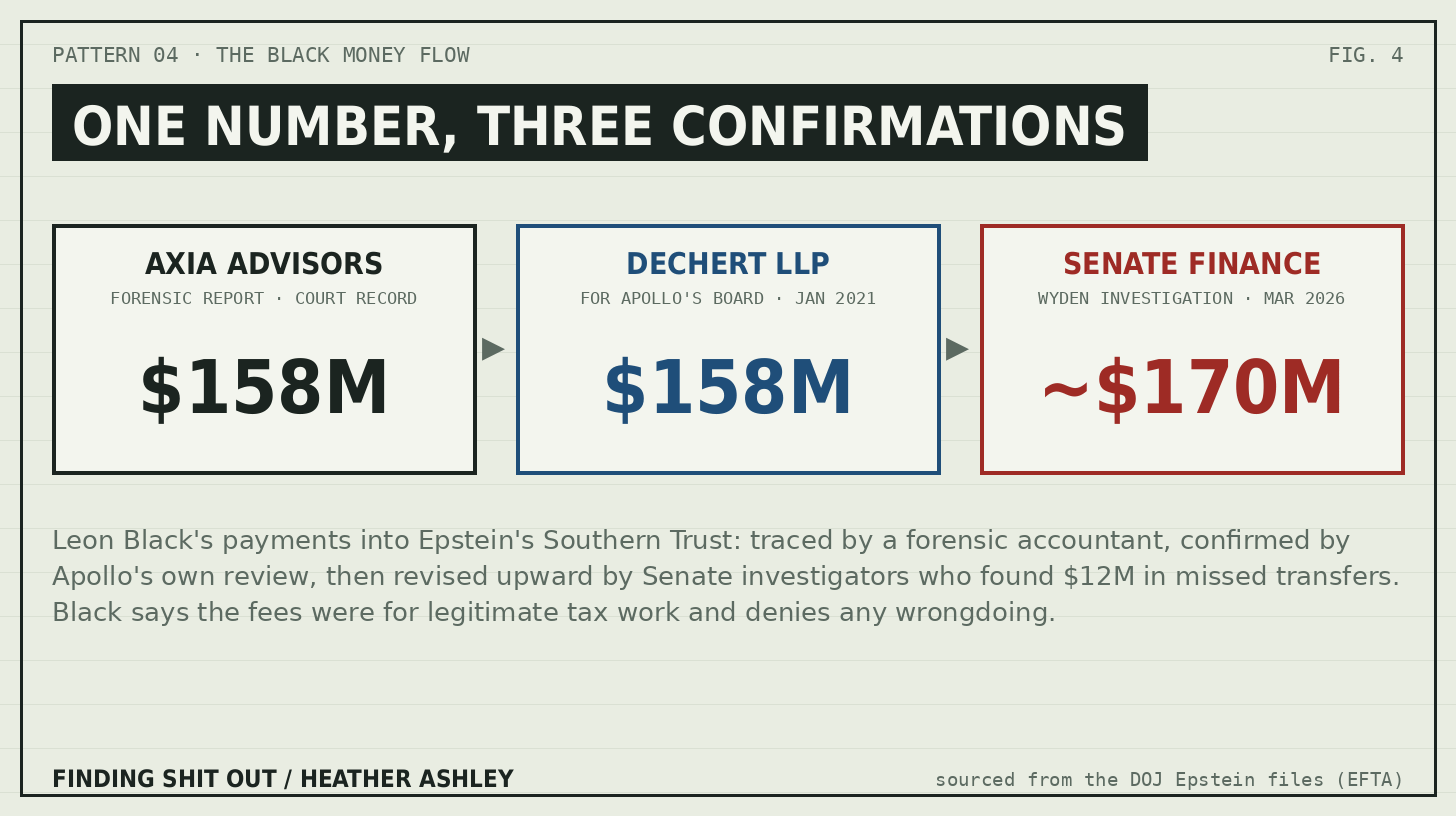

The number that anchors the whole financial picture comes from a forensic report by Axia Advisors in the court record: Of Southern Trust Company’s total revenue, $158 million came from a single source - Leon Black - including individual wires of $15 million and $16.5 million in early 2013.

Here’s what makes that figure unusual in this story: It has been independently confirmed twice. The Dechert LLP review commissioned by Apollo Global Management’s own board, reached the same $158 million conclusion (2012–2017) in January 2021. However, in March 2026, the Senate Finance Committee revised the figure upward to roughly $170 million, after investigators found about $12 million in transfers the Dechert review had missed.

A forensic accountant, the payer’s own lawyers, and a Senate committee, working separately, all landed on the same money flow - and the only correction ever made was upward.

Black has consistently said the payments were for legitimate tax and estate planning work and denies any knowledge of or involvement in Epstein’s crimes. But the flow itself is about as well-established as any fact in this entire compilation. And the loop it forms is remarkable on its face: Black wired nine figures into Epstein’s Southern Trust, while Epstein’s Southern Financial LLC - Southern Trust’s wholly owned subsidiary, per the NYDFS consent order - put $4.999 million into Apollo, the firm Black co-founded (EFTA00811539).

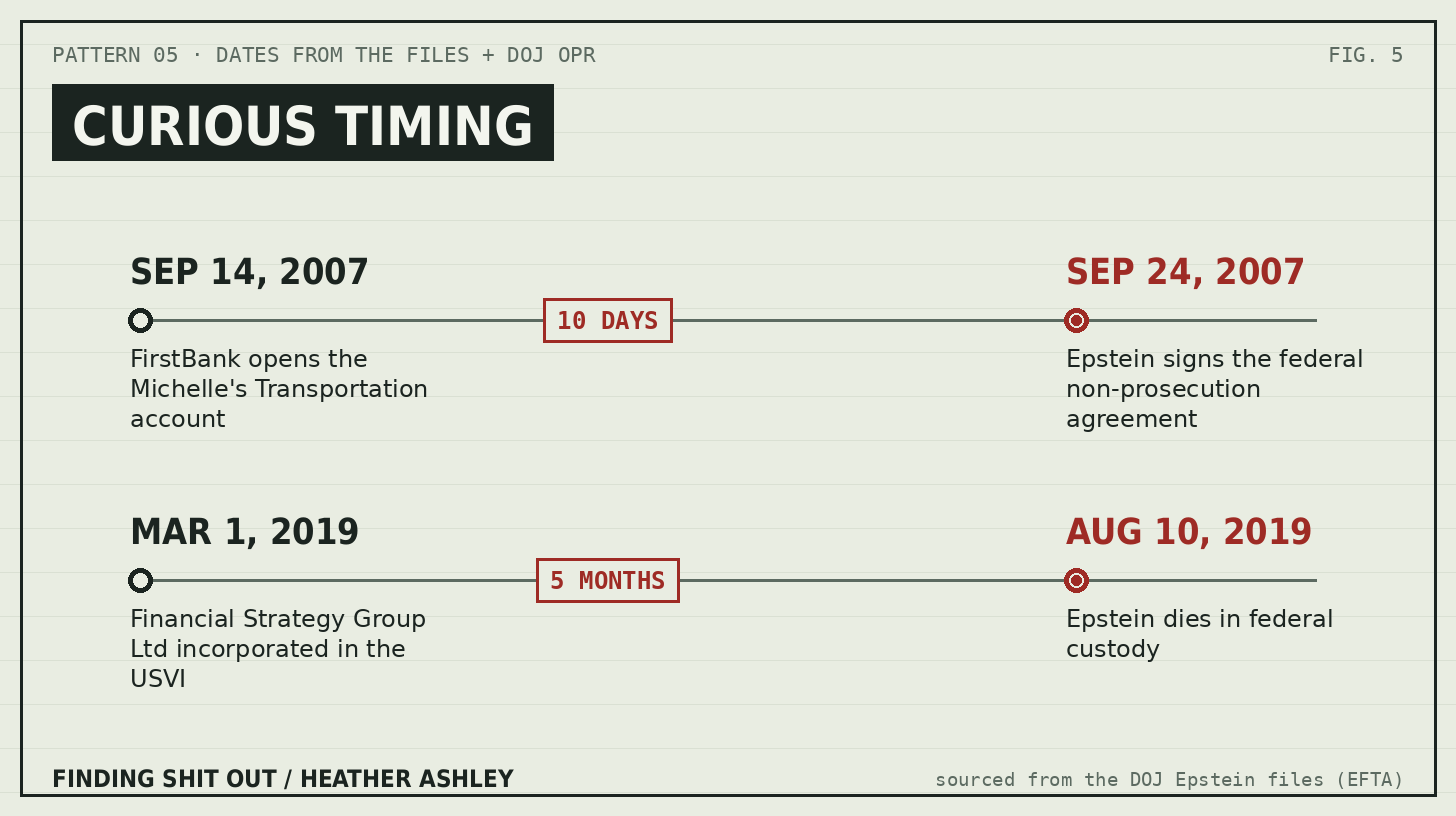

5. The dates do a lot of talking

Two pieces of timing from the files, side by side with the public record:

FirstBank opened an account for Michelle’s Transportation Co LLC on September 14, 2007. Epstein signed his federal non-prosecution agreement on September 24, 2007 - ten days later. (The NPA date isn’t my claim; it’s confirmed in the DOJ Office of Professional Responsibility’s report.) Per class-action filings, that account went on to receive $380,000 from Epstein’s personal Deutsche Bank accounts.

Financial Strategy Group Ltd was incorporated in the Virgin Islands on March 1, 2019 (EFTA00128844) - a brand-new international financial-services entity, created roughly five months before Epstein died in federal custody that August. The web continued to grow until the very end.

Timing can be circumstantial by nature, and I won’t pretend otherwise. But when a man’s corporate paperwork clusters around the most legally dangerous moments of his life, the clustering itself is a documented fact worth adding to the record.

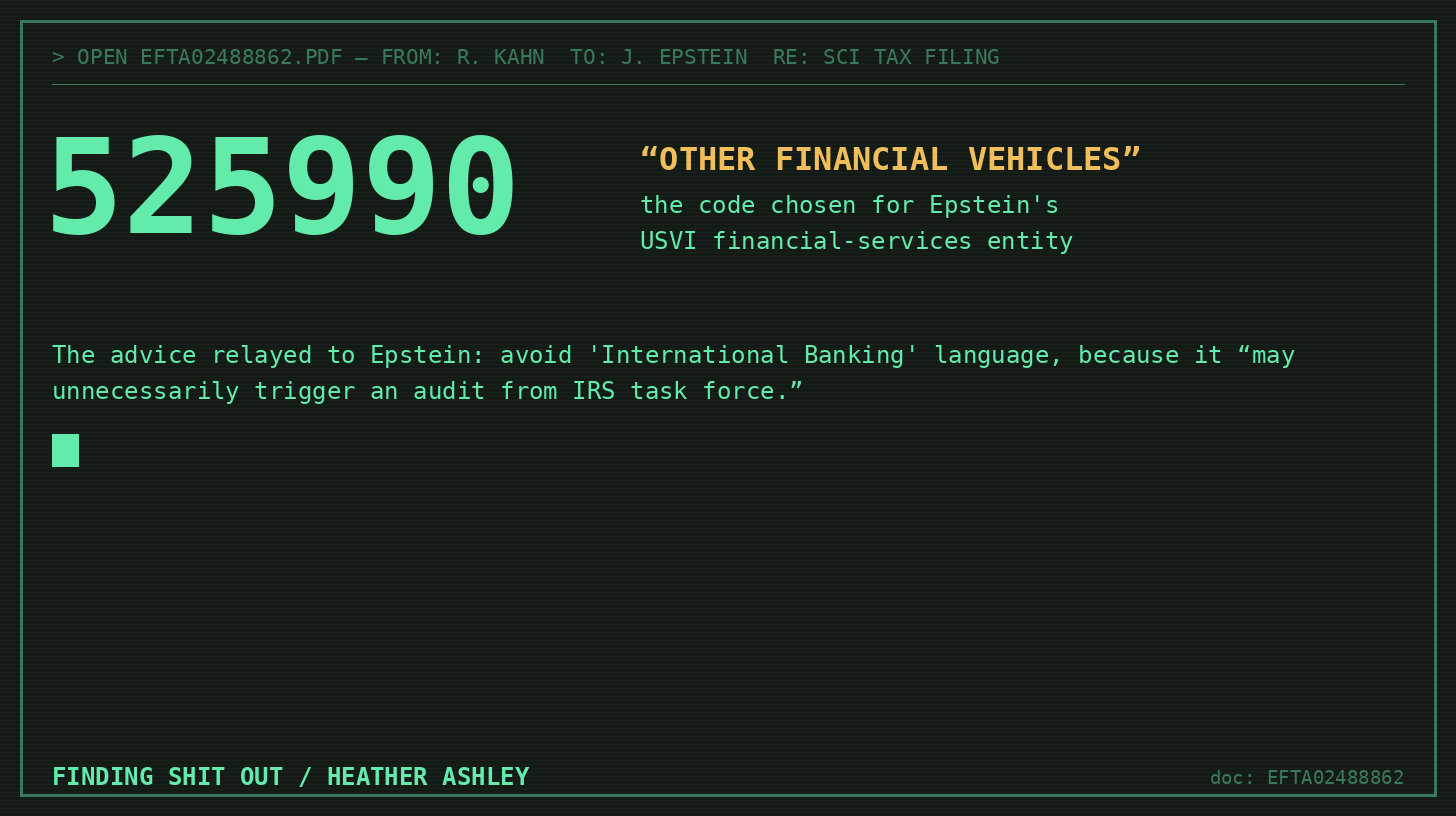

Bonus pattern: The tax code that said the quiet part out loud.

One document that stopped me in my tracks: EFTA02488862, an email in which Epstein’s accountant relays advice from tax adviser Alan Dlugash, about how to classify Southern Country International - an entity licensed in the USVI as an international financial-services operation. The recommendation was business activity code 525990, “other financial vehicles,” because including “International Banking” language “may unnecessarily trigger an audit from IRS task force.”

Read that again. The entity’s own paperwork was chosen to keep the IRS from looking too closely at what the entity was licensed to do. That’s not a pattern I inferred. It’s a documented strategy someone typed out and hit send on.

The method, one more time

None of this makes anyone in these documents guilty of anything. Officers, registered agents, and managers appear on corporate filings for entirely mundane reasons every day, and several of the people named here have denied wrongdoing and/or never been charged with any. That’s exactly why the FACT/ALLEGED distinction runs through everything I publish, until that changes: The signatures, addresses, dates, and dollar amounts above are documented; the characterizations of what they meant are, in several cases, still being fought over in courtrooms and committee hearings.

But documentation compounds. Forty entities become two addresses become six signatures become one man - and a money trail that three independent processes have now confirmed. The web was never mysterious. It was just paperwork, waiting for someone to read all of it.

The full entity-by-entity reference — with every source hyperlinked - can be found here. If you find an entity I’ve missed, my inbox is open.

Access to my research will always be free, because I don’t think anyone should have to pay for important information - but if you’d like to support my work in any way, please consider subscribing.

You’re doing similar work as @theleahfiles 😱 Together, y’all could do massive things 🙏

Based on others work - corporations in USVI can pay little to no income tax.

And I’m wondering if corporate ownership of residential property is done so you can sell the property without selling the property - you change ownership of the corporation. It’s not like a trust where you are making it easier to deal with in terms of death. That is one advantage but not the only for corporate ownership.